Best Car Insurance Policy in the USA 2026: What I Learned After My Rate Jumped $80 a Month for No Reason

I stared at my renewal notice twice, thinking I was misreading it. Same car, same clean driving record, zero tickets, zero claims, and somehow my premium had jumped almost $80 a month. No warning, no explanation, just a bigger number.

If that’s ever happened to you, you already know the sinking feeling. And if it hasn’t happened yet, it probably will, because this is happening to drivers across the entire country right now, not just me. Stick with me here, because what I found out after that renewal notice actually saved me real money, and it’ll take you ten minutes to apply the same steps.

This isn’t a “what is car insurance” article. This is exactly what I did after that renewal shock, what I learned comparing companies side by side, and what I’d tell a friend who just opened their own uncomfortable renewal email. I’m sharing this here on Insurance Pikr because this is the kind of practical, no-fluff breakdown I wish I’d found before I started shopping around myself.

Why Rates Keep Climbing (Even for Good Drivers)

A few things are driving this, and none of them are really about you personally. Repair costs have gone up because modern cars are loaded with sensors, cameras, and computer-controlled parts, so even a minor fender bender costs more to fix than it used to. Medical and legal costs tied to claims have risen too.

Nationally, full-coverage premiums are averaging somewhere between $186 and $194 a month right now, according to data from comparison sites that track real-time quotes. That number swings a lot by state, driving record, and vehicle type, but it gives you a benchmark to measure your own renewal against.

None of the reasons behind rising rates are something you can control. What you can control is whether you’re overpaying relative to what a different insurer would charge for identical coverage, and that gap is often bigger than people expect.

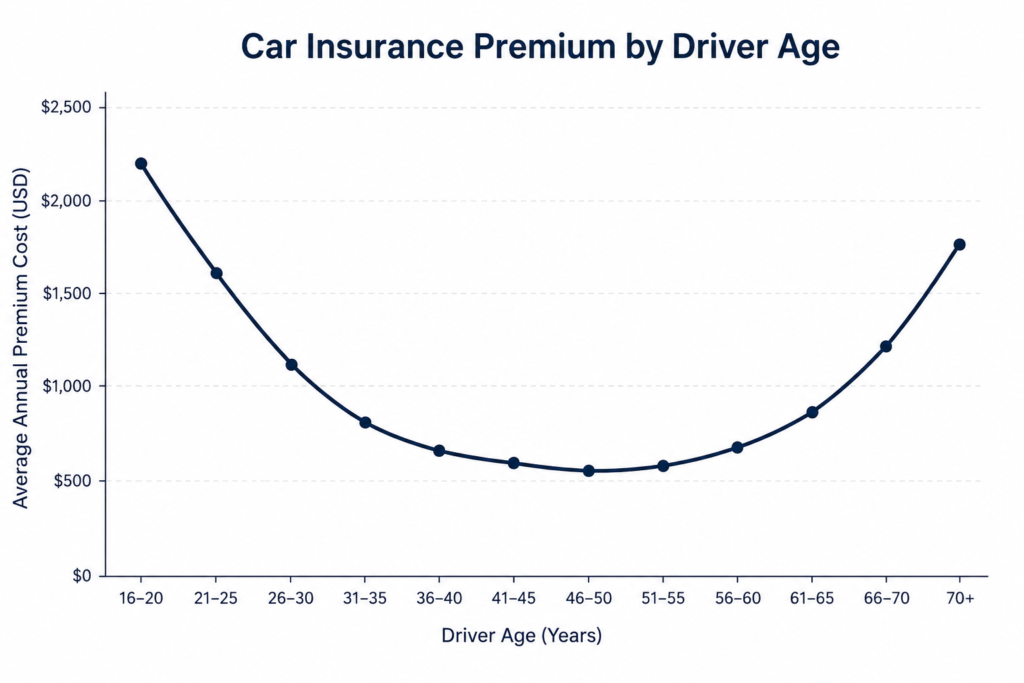

Age plays a bigger role than most people realize too. Here’s roughly how average full-coverage premiums shift over a driver’s lifetime:

| Age Group | Avg. Monthly Premium | Why |

|---|---|---|

| 16-19 | $350-450 | Highest risk category, least experience |

| 20-25 | $220-280 | Still elevated, drops as record builds |

| 26-40 | $150-190 | Typically the lowest rates of any age group |

| 41-60 | $140-175 | Stable, often the cheapest bracket |

| 61-70+ | $170-220 | Rises again due to slower reaction times, per insurer risk models |

This is also exactly why planning ahead matters, the same way I’d tell someone to lock in a life insurance policy while they’re young and healthy, getting your driving record clean early and staying with good coverage habits pays off in lower auto premiums for decades.

Liability-Only vs. Full Coverage (Get This Right First)

Before comparing companies, you need to know which type of coverage you actually need, since this affects price more than almost anything else.

- Liability-only: Covers damage and injuries you cause to others. It’s the legal minimum in nearly every state (New Hampshire and Virginia are exceptions). It does not cover your own car at all.

- Full coverage: Liability plus collision and comprehensive, meaning your own vehicle is covered too, whether from an accident, theft, weather damage, or hitting a deer.

If you’re financing or leasing your car, your lender will require full coverage regardless. If you own an older car outright and wouldn’t bother repairing it after a serious accident, dropping to liability-only (or skipping collision/comprehensive) can genuinely make sense financially.

For a deeper breakdown of state-by-state minimum coverage laws, U.S. News’ best car insurance companies guide is a solid unbiased place to check your specific state’s requirements before you decide.

Companies I Actually Looked At (and What Stood Out)

I didn’t just grab whichever name I recognized from commercials. I compared based on price, claims satisfaction, and digital tools, the same factors real comparison sites use when they rank the best car insurance companies of 2026:

- State Farm is the largest auto insurer in the country by a wide margin, insuring close to 1 in 5 U.S. drivers. Strong nationwide availability and solid discount options, though renewal price creep is a common complaint among long-time customers.

- GEICO consistently ranks well for discount variety and has a well-rated mobile app for managing policies and filing claims on the go.

- Amica ranks near the top for claims satisfaction and customer experience across multiple independent studies, though it’s rarely the cheapest option upfront. NerdWallet’s July 2026 analysis currently ranks Amica as its top overall pick for exactly this reason, strong service outweighing a higher price tag.

- Progressive stands out for coverage customization, including add-ons like gap coverage and rideshare protection.

- Travelers frequently comes up as one of the more affordable options among top-rated insurers, especially if you value price over top-tier customer satisfaction scores.

- USAA consistently scores extremely well but is only available to military members, veterans, and their families, worth checking if you qualify, since perks like deployment-related vehicle storage discounts aren’t something other insurers offer at all.

No single company is “the best” for everyone. The right one depends on whether you’re prioritizing price, claims handling, or specific discounts you personally qualify for. If cheap premiums are your main priority, Insurify’s cheapest car insurance companies breakdown is worth a look since it tracks real-time quotes across hundreds of insurers rather than static averages.

Here’s how the main options stack up side by side, based on what I found comparing them:

| Company | Best For | Avg. Monthly Rate (Full Coverage) | A.M. Best Rating | Standout Feature |

|---|---|---|---|---|

| State Farm | Nationwide availability | ~$170-190 | A++ | Largest network of local agents |

| GEICO | Discount variety | ~$150-175 | A++ | Highly rated mobile app |

| Amica | Claims satisfaction | ~$260-270 | A+ | Dividend policy option |

| Progressive | Coverage customization | ~$180-210 | A+ | Rideshare & gap coverage add-ons |

| Travelers | Affordability | ~$150-170 | A++ | Consistently low base rates |

| USAA | Military families | ~$140-160 | A++ | Deployment-specific discounts |

Step-by-Step: How I Actually Lowered My Rate

1. Pull quotes from at least 3-4 companies, not just one. I used an online comparison tool to get several quotes side by side instead of calling each insurer individually. It saved a lot of time and made the price differences obvious immediately. The Zebra’s quote comparison tool is one of the more straightforward options if you want to see multiple insurers at once without creating separate accounts everywhere.

2. Ask about every discount you might qualify for. Multi-policy bundling (home and auto together, something I also cover in my home insurance guide since bundling discounts often run 15-20%), good student, low-mileage, safe driver programs, paperless billing, and anti-theft devices all stack. I didn’t realize how many I qualified for until I actually asked instead of assuming my current insurer had already applied them automatically.

3. Consider a usage-based or pay-per-mile program if you don’t drive much. If you work from home or have a short commute, telematics programs that track your driving, or simply charge based on miles driven, can meaningfully lower your premium versus a standard flat-rate policy. This is one of the more underused ways to cut costs, and it’s exactly the kind of detail that gets buried in most generic insurance guides but genuinely moves the needle on your bill.

4. Check the insurer’s financial strength rating. An A.M. Best rating of A or higher tells you the company is financially stable enough to actually pay out claims reliably, not just offer a cheap quote today.

5. Review your deductible. A higher deductible lowers your monthly premium, but make sure it’s an amount you could actually pay out of pocket if you needed to file a claim tomorrow.

6. Re-shop every renewal, not just when something feels off. Multiple independent studies have found that drivers who switch providers at renewal save a meaningful amount annually compared to those who auto-renew without checking. I now set a calendar reminder to compare quotes about a month before my policy renews, every single year, no exceptions.

What About Students, Military, International Drivers, and USPS Employees?

A lot of people searching for car insurance don’t fit the standard “one adult, one car” profile, so here’s what’s actually relevant for a few common situations, since most generic guides skip this entirely.

Students: Good student discounts (usually requiring a B average or better) can meaningfully lower premiums for young drivers. Staying on a parent’s policy instead of a separate one is almost always cheaper if that’s an option available to you.

Military members and veterans: USAA is the standout here if you’re eligible, but several other major insurers also offer military-specific discounts even if you don’t qualify for USAA membership.

International drivers or new immigrants: Most insurers will ask for a valid U.S. driver’s license and proof of a prior driving record if available. Without U.S. driving history, rates often start higher until you build a domestic track record. Some insurers are noticeably more flexible about accepting foreign driving history than others, so it’s worth getting quotes from a few before assuming you’re stuck with the first offer you receive.

Government and USPS employees: A handful of insurers offer specific discount programs for federal and postal employees. It’s worth directly asking any insurer you’re quoting whether this applies, since it’s not always advertised upfront on their website.

Quick Checklist Before You Buy or Renew

Before you sign anything, run through this:

- [ ] Confirmed whether you need liability-only or full coverage

- [ ] Pulled quotes from at least 3-4 companies

- [ ] Asked about every discount (bundling, good student, low-mileage, anti-theft)

- [ ] Checked the insurer’s A.M. Best rating (A or higher)

- [ ] Reviewed your deductible against what you could actually afford out of pocket

- [ ] Checked if a usage-based or pay-per-mile program fits your driving habits

- [ ] Set a calendar reminder to re-shop before next year’s renewal

Common Mistakes I’d Tell Anyone to Avoid

- Auto-renewing without comparing quotes. Loyalty rarely gets rewarded with a better rate in this industry, no matter how long you’ve been a customer.

- Choosing liability-only on a car you can’t afford to replace. If losing the car entirely would hurt financially, full coverage is worth the extra monthly cost.

- Not reporting a change in mileage or usage. If you started working from home and drive far less than before, your insurer may lower your premium if you actually tell them.

- Ignoring claims satisfaction data and focusing only on price. ValuePenguin’s insurer comparison scores companies on more than just cost for exactly this reason, the cheapest quote doesn’t matter much if the company is slow or difficult when you actually need to file a claim.

- Forgetting to remove coverage on a car you no longer own. Sounds obvious, but it happens more often than you’d think after a trade-in or private sale.

Where This Leaves Me Now

I ended up switching insurers and brought my premium down close to where it was before that jump, while actually picking up a couple of discounts I didn’t have before. The renewal notice that annoyed me turned into the push I needed to stop paying for loyalty that wasn’t being rewarded with anything in return.

If your own renewal just came in higher than expected, that’s usually reason enough to get a few real quotes before just paying it without question. I put together this whole breakdown on Insurance Pikr because I wanted the guide I wish I’d had before my own renewal shock, something that actually explains the “why” instead of just listing company names.

If you’re also working through other coverage decisions around the same time, I’ve written about my own experience with life insurance, health insurance, and business insurance here on Insurance Pikr too.

For state-specific minimum coverage requirements and general auto insurance guidance, the Insurance Information Institute is a solid, unbiased reference to double-check details before you commit to a policy.

I write about this kind of practical, real-world insurance stuff regularly over on Insurance Pikr, so if this helped, there’s more where it came from.