Best Health Insurance in USA 2026: What I Learned After Picking the Wrong Plan Twice

Open enrollment used to stress me out so much that I’d just pick whatever plan I had the year before and click through as fast as possible. That worked out fine until the year I actually needed my insurance, a torn meniscus from a weekend basketball game, and found out my plan had a massive deductible I never bothered to check.

$2,400 out of pocket later, I started actually reading these plans instead of speed-clicking through Healthcare.gov every November.

This isn’t a “what is health insurance” article. This is what I actually learned comparing plans, switching providers, and figuring out which company and plan type genuinely made sense for my situation, plus what I found out helping a friend on an H1B visa and my cousin who’s an international student figure out their own coverage.

Why Health Insurance Shopping Feels Different in 2026

If you’ve checked marketplace prices recently, you’ve probably noticed premiums climbing again. Unsubsidized ACA marketplace plans are averaging around $590 a month this year, though that number swings a lot depending on your age, state, and metal tier. A bronze plan for a 30-year-old runs closer to $413 a month on average, while gold and platinum tiers cost more upfront but cover a bigger share of your medical bills.

Here’s the part that trips people up every year: cheaper premium does not mean cheaper overall cost. My torn meniscus year, I had a “cheap” plan with a sky-high deductible. I paid less monthly but got wrecked the one time I actually used it.

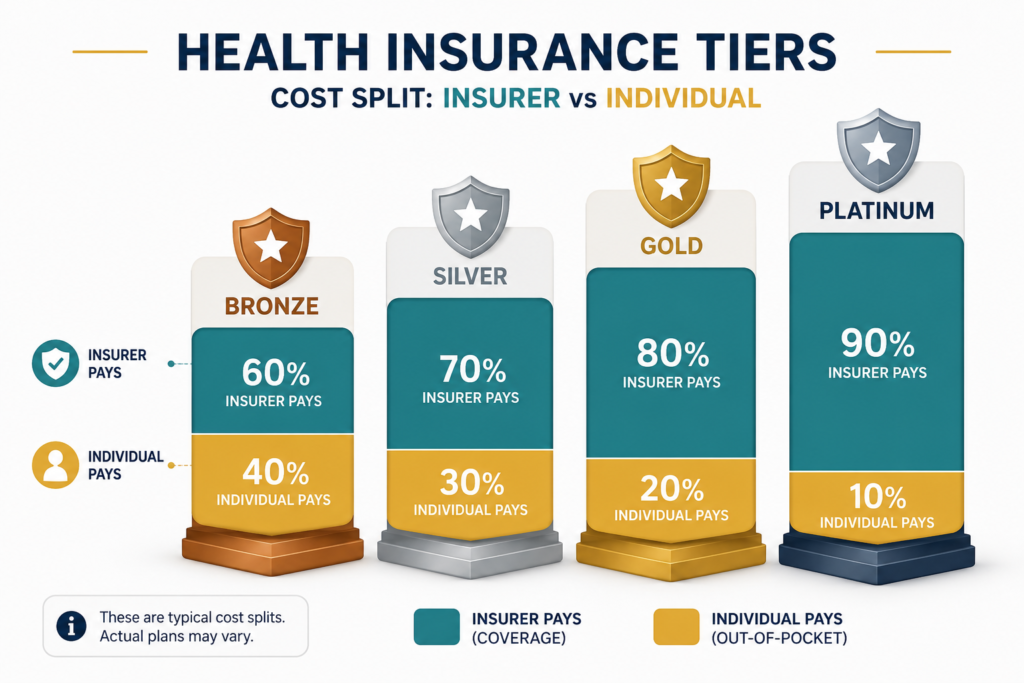

Understanding the Metal Tiers (This Actually Matters)

The ACA marketplace splits plans into four tiers: bronze, silver, gold, and platinum. The tier tells you how costs are split between you and the insurer, not how “good” the doctors are.

- Bronze: Lowest monthly premium, highest out-of-pocket costs. Insurer typically covers about 60% of costs after your deductible, you cover 40%. Makes sense if you’re healthy and rarely see a doctor.

- Silver: The most commonly picked tier. Roughly a 70/30 split. This is also the tier that unlocks extra subsidies (cost-sharing reductions) if your income qualifies.

- Gold/Platinum: Higher premiums, but the insurer covers a bigger share (80-90%) of costs. Better if you have ongoing prescriptions or expect regular care.

I switched from bronze to silver after my injury, paid maybe $60 more a month, and it would have saved me over a thousand dollars during that meniscus claim alone.

Which Companies Actually Rank Well in 2026

I dug through customer satisfaction data and complaint ratios (states track this through their insurance departments) instead of just going with whichever name I recognized. Here’s what stood out:

- Kaiser Permanente consistently ranks at the top for member satisfaction, mainly because their integrated model means your doctors and insurer are basically the same system, less back-and-forth on approvals.

- Blue Cross Blue Shield has the widest nationwide network, useful if you travel a lot or split time between states.

- UnitedHealthcare has the largest overall provider network in the country and tends to offer more flexible PPO options on the marketplace than most competitors.

- Humana is strong for Medicare-focused plans, especially for people 65+, though they’ve scaled back ACA marketplace offerings in some states.

- Molina Healthcare and Ambetter are worth checking if you qualify for subsidies, they consistently show up among the lowest-premium options for subsidy-eligible shoppers.

- Aetna and Cigna tend to have lower complaint rates and solid digital tools if you like managing everything from an app.

No single company wins every category. The “best” one really depends on whether you care more about network size, low premiums, or claims handling.

Step-by-Step: How I Actually Compare Plans Now

1. Check your actual doctors and prescriptions first. Before looking at price, I search each plan’s provider directory for my regular doctor and pharmacy. A cheap plan that doesn’t include my doctor isn’t actually cheap.

2. Calculate the realistic total cost, not just the premium. Premium plus expected out-of-pocket costs based on how much care you actually use in a normal year. HealthCare.gov’s marketplace calculator helps estimate this before you commit.

3. Check if you qualify for subsidies. Premium tax credits are available if your household income falls between 100% and 400% of the federal poverty level. This single step saved a coworker of mine almost $200 a month. Healthcare.gov has an official subsidy calculator to check your exact eligibility instead of guessing.

4. Look at the out-of-pocket maximum, not just the deductible. This is the actual ceiling on what you’d pay in a bad year. For 2026, ACA plans cap this at $9,450 for individual plans. Once you hit it, the plan covers 100% of in-network costs.

5. Compare at least 3 plans side by side before deciding. Healthcare.gov lets you do this directly. I also use eHealthInsurance to cross-check pricing since it pulls quotes from multiple carriers in one place.

What About Health Insurance for International Students, Visitors, or H1B Holders?

This part isn’t covered well anywhere, and it’s exactly what my cousin ran into when she started her master’s program here.

International students (F-1/J-1 visas): Most universities auto-enroll you in their own Student Health Insurance Plan (SHIP), which can cost $3,000 to $7,000 a year. Many schools let you waive this if you show proof of a comparable private plan, and private F-1 compliant plans often run somewhere between $1,100 and $2,000 a year instead, a real difference. Just make sure the plan meets your specific university’s waiver requirements (deductible caps, mental health coverage, evacuation benefits) before you buy anything.

Visitors (tourists, family visiting on a visa): Regular ACA marketplace plans aren’t available to short-term visitors. Instead, most people use visitor/travel medical insurance, either fixed-benefit (cheaper, capped payouts per category) or comprehensive (higher cost, no per-category caps).

H1B visa holders: Most employers include health coverage as part of the job offer, so check that first. If your employer doesn’t provide it, or you’re between jobs, short-term travel medical plans can bridge the gap, though they typically don’t cover preventive care or pre-existing conditions the way ACA plans do. Once you’ve worked in the U.S. long enough and get onto an ACA-compliant employer plan, that gap coverage isn’t needed anymore.

What About Self-Employed, Family Plans or Coverage Gaps Between Jobs?

A big chunk of people searching for health insurance aren’t W-2 employees with a simple company plan, and this part gets skipped in most guides.

Self-employed health insurance: If you’re a freelancer, gig worker, or small business owner, you’re mostly choosing between ACA Marketplace individual/family plans, a spousal plan if available, or a plan through a trade association. Since self-employed income can swing month to month, a high-deductible health plan (HDHP) paired with a Health Savings Account (HSA) is worth considering, lower premium, and you get to save pre-tax dollars for the years your income is stronger.

Family health insurance plans: Whether you go through the Marketplace or an employer, family plans bundle everyone under a shared deductible and out-of-pocket maximum, which usually works out cheaper than separate individual policies once you have more than one dependent needing regular care.

Short-term health insurance: This fills a genuine gap, between jobs, waiting for new coverage to start, or during a COBRA transition. It’s cheaper and faster to get approved, but it skips pre-existing condition coverage, maternity, and mental health care in most states, and in some states it only lasts a matter of months. Treat it strictly as a bridge, not a long-term plan.

Group vs. individual health insurance: If your employer offers a group plan, it’s usually the cheaper route since your employer covers part of the premium and the risk pool is larger. Going individual only tends to make sense if you’re self-employed, your employer’s plan is genuinely weak, or you qualify for strong ACA subsidies that beat what your workplace offers.

Small business owners: If you’re on the other side of this, offering coverage to employees, an ICHRA (Individual Coverage Health Reimbursement Arrangement) lets you reimburse employees for their own individual Marketplace plans tax-free instead of managing a traditional group policy. Worth a look if you have under 50 employees and want more budget flexibility.

What People Are Actually Asking (Reddit Threads Confirm This)

Browsing r/HealthInsurance while researching this, the same few questions come up constantly:

- “Is the cheapest plan ever actually worth it?” Rarely, unless you genuinely never see a doctor. Check your deductible and out-of-pocket max before deciding based on premium alone.

- “Can I switch plans outside open enrollment?” Only with a qualifying life event (job loss, marriage, moving states, having a baby). Otherwise, you’re locked in until the next open enrollment window.

- “Why did my premium jump even though I didn’t change anything?” Insurers adjust rates yearly based on regional healthcare costs, and your subsidy amount can shift too if your income changed.

Common Mistakes I’d Tell Anyone to Avoid

- Auto-renewing without checking the new year’s premium and network. Plans change every year, and so does your subsidy eligibility.

- Ignoring the provider directory. Confirm your actual doctors are in-network before you enroll, not after your first appointment gets billed out-of-network.

- Assuming a higher premium always means better coverage. Sometimes it does, sometimes you’re just paying for a bigger brand name.

- Forgetting to report income changes. This affects your subsidy amount and can mean owing money back at tax time if you underreport.

- Not checking prescription drug formularies. If you take regular medication, confirm it’s actually covered before assuming any “good” plan will include it.

Where This Leaves Me Now

I still don’t love open enrollment season, but I stopped speed-clicking through it. Comparing the real total cost, checking my actual doctors, and understanding what tier I’m picking has saved me real money and one very unpleasant billing surprise from happening again.

If you’re shopping this year, start with HealthCare.gov to check your subsidy eligibility, then compare a few real plans side by side before deciding. And if you’re also working through home or life insurance decisions around the same time, I’ve broken down my own experience with those too: Best Life Insurance in 2026 and Best Home Insurance Policy 2026.

For official plan details, subsidy calculators, and enrollment deadlines, Healthcare.gov is the most reliable starting point.

I write about this kind of practical, real-world insurance stuff regularly over on Insurance Pikr.